Deleted

Joined: May 3, 2024 18:59:05 GMT -5

Posts: 0

|

Post by Deleted on Mar 16, 2021 13:58:32 GMT -5

I guess I can cross IRMAA off the list of things to worry about. Me, too. Don't be so sure. Many taxes meant for "the rich" included thresholds that were never indexed for inflation. This has happened with taxation of SS as well as the Alternative Minimum Tax. And if you're looking at thresholds for couples, consider the implications of becoming a widow/widower when those thresholds are cut in half. Because all your expenses including mortgage, property taxes, utilities, etc. get cut in half if you become widowed so you got more money to pay taxes. Sure they do.  |

|

CCL

Junior Associate

Joined: Jan 4, 2011 19:34:47 GMT -5

Posts: 7,599

|

Post by CCL on Mar 16, 2021 18:12:55 GMT -5

You're correct. If one of us is ever on our own, we may exceed the threshold at some point. I think we will already be taxed on the 85% of SS. I'm hoping converting to Roths will help us reduce taxes in the long run.

It was easier putting the $$$ in the accounts than it is figuring out how to take it out.

|

|

tallguy

Senior Associate

Joined: Apr 2, 2011 19:21:59 GMT -5

Posts: 14,162

|

Post by tallguy on Mar 17, 2021 23:27:10 GMT -5

Best thing I would suggest is to not put all of your eggs into any advisor basket. Keep reading on your own. There are some people here who can give good advice. There are other sites and boards where you can get good answers too. It takes more time and effort than you may think you have available right now, but nobody will ever care more about your money than you do. It is also imperative that you know at least enough to determine whether the advice you get is good or bad, or whether it is appropriate for you.

I have an advisor assigned to me through my bank, but I meet with him rarely and most of that time is not really spent on "advice." He loves that he doesn't have to dumb things down for me when we talk, and he once told my son that I could be doing his job if I had wanted to. There is no substitute for learning on your own. It is time well spent.

|

|

justme

Senior Associate

Joined: Feb 10, 2012 13:12:47 GMT -5

Posts: 14,618

|

Post by justme on Mar 17, 2021 23:37:27 GMT -5

Damn. So my add was hitting hard today and I logged into my ssa. At full retirement I'd get a pretty good amount, if you ignored it running out of its "savings" in 14 years that'd be a big help. Like likely to cover basic needs besides Healthcare looking at today's dollars.

I'm sad I likely can't count on it for that much. But hey I'm young...I can delude myself thinking all my savings will go to retirement party time (and I suppose healthcare) for a couple more years.

Though I didn't do the math of how many years left vs retiring before 67. I've got the credits. I'm a couple more years than that in. Though hoping not to work 40 years. So I guess it going broke won't be as much?

|

|

|

|

Post by minnesotapaintlady on Mar 18, 2021 7:30:33 GMT -5

justme - keep in mind that estimate assumes you work all the way up until retirement age at your current income. I think there's a calculator on the SS website where you can factor in early retirement.

|

|

Lizard Queen

Senior Associate

103/2024

Joined: Jan 17, 2011 22:19:13 GMT -5

Posts: 14,659

|

Post by Lizard Queen on Mar 18, 2021 9:13:13 GMT -5

You could also see what the smart people at mrmoneymustache forum have to say. They seem to live for that stuff.

|

|

susana1954

Well-Known Member

Joined: Feb 23, 2021 18:50:55 GMT -5

Posts: 1,398

|

Post by susana1954 on Mar 18, 2021 10:13:03 GMT -5

I will tell you guys who are in your 40s or so that what looks like decent money now to live on may not be if a high rate if inflation rears its ugly head. And the way the U.S. is pumping $$$ into circulation, that's almost a given. Inflation is a factor. If you earn $60k now, you might need to figure that you need almost $90k in 20 years with a 2% inflation rate. Inflation has been relatively low in the past 20 years, but it has still averaged 2% from 2000-2020. And that's before the stimulus payments. Anyway, here's a calculator that will tell you how much you will need based to replace whatever amount that you think you will need to live on. You can change the inflation rate, which is what I did to come up with the figure above. link |

|

Deleted

Joined: May 3, 2024 18:59:05 GMT -5

Posts: 0

|

Post by Deleted on Mar 18, 2021 10:26:02 GMT -5

Inflation is a factor. If you earn $60k now, you might need to figure that you need almost $90k in 20 years with a 2% inflation rate. Inflation has been relatively low in the past 20 years, but it has still averaged 2% from 2000-2020. I once saw a post on crediboards_dot_com from someone who figured that $1 million would be enough for retirement- invest it at 8%, draw off $80K/year and you're all set. Yes, I DID respond and point out the effects of inflation ($80K won't buy as much in 20 years as it will right now) and that for many retirees, an 8% yield means you're too aggressively invested in equities and and that an 8% return comes with volatility. For me, the most important metric is my annual increase in assets since retirement AFTER withdrawals and it's currently running over 4%. That's a new high and I expect it to come down but it means that I can withdraw larger dollar amounts in the future to keep up with inflation without running out of money. |

|

|

|

Post by minnesotapaintlady on Mar 18, 2021 11:17:53 GMT -5

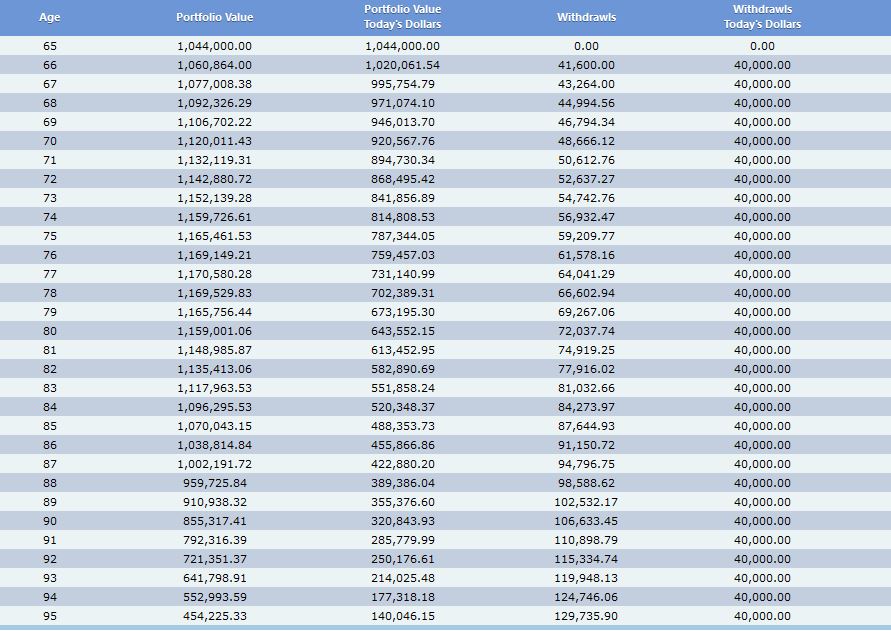

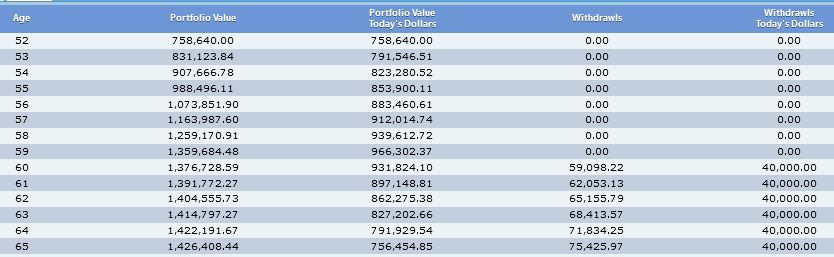

I will tell you guys who are in your 40s or so that what looks like decent money now to live on may not be if a high rate if inflation rears its ugly head. And the way the U.S. is pumping $$$ into circulation, that's almost a given. Inflation is a factor. If you earn $60k now, you might need to figure that you need almost $90k in 20 years with a 2% inflation rate. Inflation has been relatively low in the past 20 years, but it has still averaged 2% from 2000-2020. And that's before the stimulus payments. Anyway, here's a calculator that will tell you how much you will need based to replace whatever amount that you think you will need to live on. You can change the inflation rate, which is what I did to come up with the figure above. linkI don't know about everyone else here, but when I say 40K/year I mean in today's dollars, not what I'd actually withdraw every year. This chart is assuming 5% inflation and a 60/40 portfolio with the stocks returning 8% and the fixed income at 2%

|

|

susana1954

Well-Known Member

Joined: Feb 23, 2021 18:50:55 GMT -5

Posts: 1,398

|

Post by susana1954 on Mar 18, 2021 14:35:51 GMT -5

I will tell you guys who are in your 40s or so that what looks like decent money now to live on may not be if a high rate if inflation rears its ugly head. And the way the U.S. is pumping $$$ into circulation, that's almost a given. Inflation is a factor. If you earn $60k now, you might need to figure that you need almost $90k in 20 years with a 2% inflation rate. Inflation has been relatively low in the past 20 years, but it has still averaged 2% from 2000-2020. And that's before the stimulus payments. Anyway, here's a calculator that will tell you how much you will need based to replace whatever amount that you think you will need to live on. You can change the inflation rate, which is what I did to come up with the figure above. linkI don't know about everyone else here, but when I say 40K/year I mean in today's dollars, not what I'd actually withdraw every year. This chart is assuming 5% inflation and a 60/40 portfolio with the stocks returning 8% and the fixed income at 2%

Yes, but you can't use the term "today's dollars" and "future dollars" interchangeably. $41k in 2041 won't buy what 41k will in 2021. So unless you are now 65 years old, your chart overestimates when the chart says it will only take $41k to buy what you could buy in 2020 for $40k. You need to figure out how big your portfolio needs to be so that you can withdraw the equivalent of $40k in today's dollars (assuming 2% inflation) when you are 66. Then the chart would be more accurate. The calculator I linked says you should be withdrawing the equivalent of $40k in 2041 if you have a portfolio of $1,485,94k and withdraw $59k. That's hoping for a low rate of inflation, though. This is why I can't afford to take withdrawals from my IRA until RMDs kick in. There is no automatic COLA to my pension, and the last increase was fifteen years ago. An increase takes an act of the legislature. |

|

Lizard Queen

Senior Associate

103/2024

Joined: Jan 17, 2011 22:19:13 GMT -5

Posts: 14,659

|

Post by Lizard Queen on Mar 18, 2021 14:46:27 GMT -5

I don't know about everyone else here, but when I say 40K/year I mean in today's dollars, not what I'd actually withdraw every year. This chart is assuming 5% inflation and a 60/40 portfolio with the stocks returning 8% and the fixed income at 2%

Yes, but you can't use the term "today's dollars" and "future dollars" interchangeably. $41k in 2041 won't buy what 41k will in 2021. So unless you are now 65 years old, your chart overestimates when it says it will only take $41k to buy what you could buy in 2020. Look at the withdrawals column. |

|

susana1954

Well-Known Member

Joined: Feb 23, 2021 18:50:55 GMT -5

Posts: 1,398

|

Post by susana1954 on Mar 18, 2021 14:48:35 GMT -5

Yes, but you can't use the term "today's dollars" and "future dollars" interchangeably. $41k in 2041 won't buy what 41k will in 2021. So unless you are now 65 years old, your chart overestimates when it says it will only take $41k to buy what you could buy in 2020. Look at the withdrawals column. I did. It is the starting point that is questionable. This is great for someone who will retire in 2022. I don't think that describes most of you. |

|

Happy prose

Senior Member

Joined: Dec 20, 2010 12:55:24 GMT -5

Posts: 3,228

|

Post by Happy prose on Mar 18, 2021 14:59:16 GMT -5

Would it make sense to make an appointment with an accountant? I don't really want to meet a financial advisor. Wouldn't an accountant be able to tell you the ins and outs, without trying to sell you stuff? I don't know why, but the thought of a financial advisor intimidates me.

|

|

Lizard Queen

Senior Associate

103/2024

Joined: Jan 17, 2011 22:19:13 GMT -5

Posts: 14,659

|

Post by Lizard Queen on Mar 18, 2021 15:11:07 GMT -5

Look at the withdrawals column. I did. It is the starting point that is questionable. This is great for someone who will retire in 2022. I don't think that describes most of you. Oh! I see what you're saying now. Yeah, we're padding our final number due to that. Even if people aren't, they are going to look at that number at the point when they retire. Everything in between is just guess work. |

|

|

|

Post by minnesotapaintlady on Mar 18, 2021 15:28:01 GMT -5

Look at the withdrawals column. I did. It is the starting point that is questionable. This is great for someone who will retire in 2022. I don't think that describes most of you. I just used that to illustrate that even with 5% inflation built into the withdrawals a 4% draw down could keep you at 40K spending power in today's dollars all through retirement.

I have been "guessing" 35-40K for a long time, the closer I get, the more confident I am. But really...looking at my SS statement, my income has been pretty flat since the mid 90's, so I have a hard time fathoming that I'll need 50% more in 7 years than I do now.  |

|

Lizard Queen

Senior Associate

103/2024

Joined: Jan 17, 2011 22:19:13 GMT -5

Posts: 14,659

|

Post by Lizard Queen on Mar 18, 2021 15:40:07 GMT -5

The prior talk over RMDs has me worried now. Can we go back in time 3 months so that I can withdraw more from my inherited IRA? My MRD for that suddenly jumped to $5600. I was expecting $1000 less. I suppose I could do a lot of number crunching to project that one out into the future. I guess its good that I took a distribution last year, but it could have been 10's of thousands more, and still stayed in the 12% tax range.

|

|

justme

Senior Associate

Joined: Feb 10, 2012 13:12:47 GMT -5

Posts: 14,618

|

Post by justme on Mar 18, 2021 16:23:00 GMT -5

Would it make sense to make an appointment with an accountant? I don't really want to meet a financial advisor. Wouldn't an accountant be able to tell you the ins and outs, without trying to sell you stuff? I don't know why, but the thought of a financial advisor intimidates me. That's not in the wheelhouse of the accountants I know. They're pretty much strictly taxes and balance sheets. (There's a bit more in there) Not investments and such. There are advisers out there that are fee-only so they're not interested in selling you anything because you're paying them for advice vs others that only make commissions. I think CFPs are that but I'm not sure if they all are. Search for fee-only financial planners/advisors in your area. It might cost you a few hundred depending on area/how complex your situation is. |

|

justme

Senior Associate

Joined: Feb 10, 2012 13:12:47 GMT -5

Posts: 14,618

|

Post by justme on Mar 18, 2021 16:23:59 GMT -5

justme - keep in mind that estimate assumes you work all the way up until retirement age at your current income. I think there's a calculator on the SS website where you can factor in early retirement. Yeah, that's what my last line of my post was trying to say but failed to adequately say it. |

|

saveinla

Junior Associate

Joined: Dec 19, 2010 2:00:29 GMT -5

Posts: 5,227

|

Post by saveinla on Mar 18, 2021 16:48:08 GMT -5

justme - keep in mind that estimate assumes you work all the way up until retirement age at your current income. I think there's a calculator on the SS website where you can factor in early retirement. Yeah, that's what my last line of my post was trying to say but failed to adequately say it. But after a certain point, the amount you get does not change much even if you earn the same or not. I think we had a discussion about the bend points a while ago. |

|

justme

Senior Associate

Joined: Feb 10, 2012 13:12:47 GMT -5

Posts: 14,618

|

Post by justme on Mar 18, 2021 18:11:46 GMT -5

Yeah, that's what my last line of my post was trying to say but failed to adequately say it. But after a certain point, the amount you get does not change much even if you earn the same or not. I think we had a discussion about the bend points a while ago. Good to know. I'm a ways off, but do hope to retire way before my retirement age. Currently only have 11 years at a full wage. Have some years of only a few thousand of earnings, but I'll definitely have some 0s if I retire before 60. Though I still have some salary jumps I should make so my future income is likely to counter balance that better. |

|

Lizard Queen

Senior Associate

103/2024

Joined: Jan 17, 2011 22:19:13 GMT -5

Posts: 14,659

|

Post by Lizard Queen on Mar 18, 2021 18:13:02 GMT -5

I can't imagine it would take that long. They probably plug numbers into a program, and it spits out a report.

|

|

Happy prose

Senior Member

Joined: Dec 20, 2010 12:55:24 GMT -5

Posts: 3,228

|

Post by Happy prose on Mar 18, 2021 19:45:01 GMT -5

That's not in the wheelhouse of the accountants I know. They're pretty much strictly taxes and balance sheets. (There's a bit more in there) Not investments and such. There are advisers out there that are fee-only so they're not interested in selling you anything because you're paying them for advice vs others that only make commissions. I think CFPs are that but I'm not sure if they all are. Search for fee-only financial planners/advisors in your area. It might cost you a few hundred depending on area/how complex your situation is. This. I have the same fear of advisors tied to any bank or corporation, Happy prose . The Garrett network is made up of independent, fee-only advisors that have a fiduciary duty to their clients. Since their only compensation is their hourly fee paid by the client, they don't have the restrictions (like minimum $1mill assets) that commission-based advisors do, and are able to work with with a more diverse array of clients. And they'll take on a 1-hour project as well as an ongoing, years-long retainer-based project. The lowest hourly rate I've seen so far is $180 in MN; my state is in the $200s; I'd bet CA and NY are much higher, but the couple I checked out of curiosity don't have their rate listed. I think those fees are reasonable--based on my limited knowledge of the extra costs of being self-employed/running your own business--but I'm not sure I'd be willing to pay for more than a day's work at that rate.

Thank you. I'm going to look this up right now. I plan to retire in 1 yr, nine months. ETA- One in NJ, close to home, $210 per hour. Not bad! |

|

Lizard Queen

Senior Associate

103/2024

Joined: Jan 17, 2011 22:19:13 GMT -5

Posts: 14,659

|

Post by Lizard Queen on Mar 18, 2021 20:08:49 GMT -5

But after a certain point, the amount you get does not change much even if you earn the same or not. I think we had a discussion about the bend points a while ago. Good to know. I'm a ways off, but do hope to retire way before my retirement age. Currently only have 11 years at a full wage. Have some years of only a few thousand of earnings, but I'll definitely have some 0s if I retire before 60. Though I still have some salary jumps I should make so my future income is likely to counter balance that better. I crunched the numbers. In order to max to the 2nd bend, you need total indexed wages for 35 years to be $2,266,740, which averages to $64,764/ year. Here's how to calculate the index: www.fool.com/retirement/social-securitys-bend-points-what-are-they.aspx |

|

TheOtherMe

Distinguished Associate

Joined: Dec 24, 2010 14:40:52 GMT -5

Posts: 27,206

Mini-Profile Name Color: e619e6

|

Post by TheOtherMe on Mar 19, 2021 8:13:41 GMT -5

At one of the small tax firms where I prepared returns, the owner was transitioning to a financial advisor firm. I did not work on that side of it, but I do know he would not talk to you if you didn't have $1,000,000 in assets. I think he charged by a % of the assets.

His financial advisor clients took priority over regular long time tax clients when it came to their tax return. He would bring it in to my office and give me a lecture about how important they were and how this return had to be 100% correct. He signed all tax returns but only did a cursory review of regular people's tax returns. He reviewed the financial advisor clients' tax returns with a fine tooth comb.

Their tax returns were included in their fees they paid him.

We were hourly employees, so it didn't matter to us.

|

|

Lizard Queen

Senior Associate

103/2024

Joined: Jan 17, 2011 22:19:13 GMT -5

Posts: 14,659

|

Post by Lizard Queen on Mar 19, 2021 9:28:46 GMT -5

Good to know. I'm a ways off, but do hope to retire way before my retirement age. Currently only have 11 years at a full wage. Have some years of only a few thousand of earnings, but I'll definitely have some 0s if I retire before 60. Though I still have some salary jumps I should make so my future income is likely to counter balance that better. I crunched the numbers. In order to max to the 2nd bend, you need total indexed wages for 35 years to be $2,266,740, which averages to $64,764/ year. Here's how to calculate the index: www.fool.com/retirement/social-securitys-bend-points-what-are-they.aspxI was using the 2018 numbers from that article. The current numbers for the second bend are $2,520,840 and $72,024/yr. |

|

teen persuasion

Senior Member

Joined: Dec 20, 2010 21:58:49 GMT -5

Posts: 4,046

|

Post by teen persuasion on Mar 20, 2021 20:45:47 GMT -5

There are some online sites that you can play with to get some ideas on how your retirement income could play out, try scenarios, optimize income streams, etc. i-ORP has a basic version and an extended version (scroll down to find that link). It tries to figure out your max smoothed retirement income. You can play with changing inputs to see what happens. FireCalc tests out your probability of having enough to spend thruout retirement. Again, can tweak more details by adding info on the extra tabs at the top. cFIREsim is a different take on FireCalc, might give different insights, or be easier to use/understand. Open Social Security figures out your optimal SS claiming strategy. You need to know your PIA at FRA. Don't get freaked out by all the fields you might not have any idea what they are talking about. Just start with the easiest versions, basic info you do know: expected SS, 401k or IRA balances, pensions, etc. Run the simulations, see what it tells you. Change a data point: taking SS earlier, or later; Roth convert some each year; change withdrawal amount up or down; change expected inflation or interest rates or stock growth rates. See what happens. Use this to test out good or bad scenarios to watch or plan for, and to see what happens to taxes. See what a different mix of Roth/traditional/taxable balances does, or which you draw from first or more heavily. Play around. |

|

Lizard Queen

Senior Associate

103/2024

Joined: Jan 17, 2011 22:19:13 GMT -5

Posts: 14,659

|

Post by Lizard Queen on Mar 20, 2021 21:17:53 GMT -5

So, in my case, I've got kids going to college around the time I might want RE, or maybe just my DH, and I keep working a few years. How does the expected family contribution work. Will we both have to continue working to pay for college?

|

|

|

|

Post by minnesotapaintlady on Mar 20, 2021 21:37:56 GMT -5

So, in my case, I've got kids going to college around the time I might want RE, or maybe just my DH, and I keep working a few years. How does the expected family contribution work. Will we both have to continue working to pay for college? EFC is based mainly on income, so if you're retired it's easier to manipulate that. They are changing the name from EFC to Student Aid Index or something like that next year because people were confused that Expected Family Contribution really MEANT expected family contribution...which it doesn't. It's really just a measure to see if you're eligible for a Pell grant and subsidized loans and if your state offers a grant they usually use the EFC to determine that as well. Also, keep in mind that FAFSA goes back 2 years. So for freshman year in college you're using your tax info from when they're second semester sophomores in high school! |

|

Lizard Queen

Senior Associate

103/2024

Joined: Jan 17, 2011 22:19:13 GMT -5

Posts: 14,659

|

Post by Lizard Queen on Mar 20, 2021 21:47:14 GMT -5

So, in my case, I've got kids going to college around the time I might want RE, or maybe just my DH, and I keep working a few years. How does the expected family contribution work. Will we both have to continue working to pay for college? EFC is based mainly on income, so if you're retired it's easier to manipulate that. They are changing the name from EFC to Student Aid Index or something like that next year because people were confused that Expected Family Contribution really MEANT expected family contribution...which it doesn't. It's really just a measure to see if you're eligible for a Pell grant and subsidized loans and if your state offers a grant they usually use the EFC to determine that as well. Also, keep in mind that FAFSA goes back 2 years. So for freshman year in college you're using your tax info from when they're second semester sophomores in high school! Yeah, we're thinking my DH may be able to retire that year, but I don't know if I could get my income down low enough so they don't look at our retirement accounts. I'm not sure about that threshold, though. |

|

|

|

Post by minnesotapaintlady on Mar 20, 2021 21:57:58 GMT -5

EFC is based mainly on income, so if you're retired it's easier to manipulate that. They are changing the name from EFC to Student Aid Index or something like that next year because people were confused that Expected Family Contribution really MEANT expected family contribution...which it doesn't. It's really just a measure to see if you're eligible for a Pell grant and subsidized loans and if your state offers a grant they usually use the EFC to determine that as well. Also, keep in mind that FAFSA goes back 2 years. So for freshman year in college you're using your tax info from when they're second semester sophomores in high school! Yeah, we're thinking my DH may be able to retire that year, but I don't know if I could get my income down low enough so they don't look at our retirement accounts. I'm not sure about that threshold, though. They never consider retirement accounts or home equity in your primary residence. If you can get AGI below 50K and don't have to file schedule 1 with your 1040 (with a few exceptions like if you need to to claim unemployment or an IRA contribution) all assets are ignored. Of course this could all change by the time you're getting serious and probably will. There's a big reform of the form coming up next year, so I'm anxious to see what that looks like. |

|