CCL

Junior Associate

Joined: Jan 4, 2011 19:34:47 GMT -5

Posts: 7,599

|

Post by CCL on Mar 11, 2021 11:25:51 GMT -5

Good to know. I go back and forth over taxable account vs. paying down the house. DH and I plowed all the retirement money into the tax deferred accounts. We avoided federal and state income tax on the deposits and had good gains on the accounts. The money grows until you actually need it. I figure the account has earned the portion to pay the IRS, probably several times over. DH began his 401k at age 25 and is now 62 so that is a lot of years of earning potential. No one wants to pay more in taxes than they have to. Everyone with an income owes the taxes due. At some point you have to face the music. Good for him! I wanted to contribute to 401k a long time before we actually did. I knew nothing about them and couldn't find any info, no Internet back then. |

|

countrygirl2

Senior Associate

Joined: Dec 7, 2016 15:45:05 GMT -5

Posts: 16,930

|

Post by countrygirl2 on Mar 11, 2021 12:10:05 GMT -5

We are hoping to take some money out this year and next and apply the tax credits from the solar to reduce our tax bill. Have to walk a fine line to see what we can do and not get a medicare penalty, may have to.

|

|

tallguy

Senior Associate

Joined: Apr 2, 2011 19:21:59 GMT -5

Posts: 14,162

|

Post by tallguy on Mar 11, 2021 13:01:58 GMT -5

Interestingly, it could be even less time than that. If you were to open the Roth IRA by the due date of your tax return it could apply to the previous tax year. It would then be well under four years actual time. If the person were to open their Roth by April 15, 2021, apply the contribution to the 2020 tax year, and take the distribution in January 2025, that would be 45 months.

|

|

|

|

Post by The Walk of the Penguin Mich on Mar 11, 2021 14:01:44 GMT -5

Good to know. I go back and forth over taxable account vs. paying down the house. DH and I plowed all the retirement money into the tax deferred accounts. We avoided federal and state income tax on the deposits and had good gains on the accounts. The money grows until you actually need it. I figure the account has earned the portion to pay the IRS, probably several times over. DH began his 401k at age 25 and is now 62 so that is a lot of years of earning potential. No one wants to pay more in taxes than they have to. Everyone with an income owes the taxes due. At some point you have to face the music.True, but RMDs can have you paying more than you would have under other conditions. Those RMDs can also put you over the IRMAA limit, where your Medicare gets surcharged as well. That increases your tax burden far more than just removing from your tax deferred accounts of what you need to live. Right now, TD's figured that if everything stays the same, we are going to be paying between $7-9K more in IRMAA between 2 Medicare payments. As a result, we are converting what we can to Roth's in order to decrease the amount of RMDs we will need to take. You really need to do the math so you don't get blindsided. |

|

bookkeeper

Well-Known Member

Joined: Mar 30, 2012 13:40:42 GMT -5

Posts: 1,697

|

Post by bookkeeper on Mar 11, 2021 15:02:30 GMT -5

Planning a withdrawal strategy and the tax implications that go along with it are very important. I didn't mean to imply it wasn't. Just like everyone's financial situation is different, so is their tax situation. That's one of the reasons I enjoy reading everyone's input here. I learn how better to manage my situation as well as what others are doing for their lives.

DH and I plan our income/expense and tax bill every November for the coming year. We can't control what happens in D.C. with the tax code, but we can attempt to control what we draw, how we draw it and what we will need to pay the IRS.

|

|

seriousthistime

Senior Member

Joined: Dec 22, 2010 20:27:07 GMT -5

Posts: 4,709

|

Post by seriousthistime on Mar 11, 2021 15:03:47 GMT -5

We are hoping to take some money out this year and next and apply the tax credits from the solar to reduce our tax bill. Have to walk a fine line to see what we can do and not get a medicare penalty, may have to. If you're talking about Medicare's IRMAA, I'm not sure the solar tax credits would help you. IRMAA is based on MAGI. I think MAGI is calculated before deductions and tax credits. The tax credits would reduce your tax bill, but I don't think they would reduce your MAGI. But I'm not an expert, so it would be good to check. |

|

Deleted

Joined: May 3, 2024 20:14:39 GMT -5

Posts: 0

|

Post by Deleted on Mar 11, 2021 16:01:26 GMT -5

We are hoping to take some money out this year and next and apply the tax credits from the solar to reduce our tax bill. Have to walk a fine line to see what we can do and not get a medicare penalty, may have to. If you're talking about Medicare's IRMAA, I'm not sure the solar tax credits would help you. IRMAA is based on MAGI. I think MAGI is calculated before deductions and tax credits. The tax credits would reduce your tax bill, but I don't think they would reduce your MAGI. But I'm not an expert, so it would be good to check. I agree. IRMAA is based on MAGI and is not affected by deductions or credits. They even add in your municipal bond interest, which is not part of your Adjusted Gross because it's not taxable by the Feds- but it can still throw you into a higher IRMAA bracket.  |

|

saveinla

Junior Associate

Joined: Dec 19, 2010 2:00:29 GMT -5

Posts: 5,227

|

Post by saveinla on Mar 11, 2021 16:11:09 GMT -5

Sorry for my ignorance, but we pay a lot of taxes during our earning years. How is that different from what we are paying in retirement?

I am really asking this question, as it seems that planning for retirement seems to be very hard if you have saved some money.

|

|

tallguy

Senior Associate

Joined: Apr 2, 2011 19:21:59 GMT -5

Posts: 14,162

|

Post by tallguy on Mar 11, 2021 16:24:20 GMT -5

There are ways to work around paying high taxes in retirement for most people. Some are just destined to pay a lot, because they have a lot. If this is you, be thankful for it. Nobody in this country pays a lot without keeping a lot more.

|

|

saveinla

Junior Associate

Joined: Dec 19, 2010 2:00:29 GMT -5

Posts: 5,227

|

Post by saveinla on Mar 11, 2021 17:06:06 GMT -5

I agree - that is why I am asking the question. I understand the details of how it works for people who don't pay a lot of taxes, but other than tax deferred 401K savings, a lot of people don't have any other option to reduce taxes right now.

I was just wondering why even people who earn more are making a lot of effort to keep income below a certain level.

|

|

buystoys

Junior Associate

Joined: Mar 30, 2012 4:58:12 GMT -5

Posts: 5,650

|

Post by buystoys on Mar 11, 2021 17:10:57 GMT -5

If you retire early and you need to purchase medical coverage on the market, you want to keep your income down in order to receive subsidies. The subsidies have a cliff to them. If you are $1 over 400% FPL, you get zero help. If you are below, you get help based on your level of income. Medical coverage can be very expensive depending on where you live. I'm not yet 60 and was paying $1000 per month for coverage with a $6500 deductible. That ate up our budget really quick.

|

|

Deleted

Joined: May 3, 2024 20:14:39 GMT -5

Posts: 0

|

Post by Deleted on Mar 11, 2021 19:16:10 GMT -5

The big thing to remember is that as long as you keep saving and investing, you will have options. Yes, some options are better than others, both now and in the future. but at least you will have some. That alone puts you far ahead of many if not most of the people in this country. Learn about Roths. See where they fit into your plan. You will not get a tax break up front on the contributions, but it should probably be much more beneficial later on. Try to forecast as much as you can what your income and expenses are going to be in retirement, and at what age you want to leave the work world. Once you are able to do that you can ask more detailed questions and make more specific plans. In other words, KISS (keep it simple stupid) until you figure out what the heck you’re doing and need to do, right?  I don’t say that in a negative way, because I think your advice is great, and I appreciate it. I’ve been meaning to learn more about Roths since I found these boards and saw you all talking about them. I just never felt a real sense of urgency, like I’m starting to feel now. I mean, at least I was saving for retirement, I thought I’d figure out the details later. Well, “later” is starting to feel like it should be “now”. And it sounds like you kind of said that I’m doing something half-way right by saving and investing in the first place, even though I haven’t figured out yet what I should have where, and I sincerely appreciate that too. I already know when I want to leave the working world. Tomorrow wouldn’t be too soon for me.😁 Realistically speaking though, I pray no later than 10 years from now. I want out literally as soon as possible, meaning whenever I can make the math make sense for the rest of my life. Without an early retirement offer with a financial incentive (which my employer has done in the past) that would be the earliest I think I can realistically retire, which is 2 years beyond when I would be eligible as far as my job goes. I’d shed real tears and be very, very unhappy if I had to work more than 10 more years. I have 6 more years before I would be eligible to take advantage of an early out with an incentive, if it was even offered. That would be awesome, but no matter what, for the love of all that is good and holy, PLEASE GOD, I don’t want to work my current job more than 10 more years. In 10 years and some months, I’ll be eligible to use the funds in my retirement account without penalty and receive my pension and the supplement. Anyway, you didn’t ask about all that. Just, thanks for the advice. |

|

Deleted

Joined: May 3, 2024 20:14:39 GMT -5

Posts: 0

|

Post by Deleted on Mar 11, 2021 19:20:26 GMT -5

I didn’t mean to bail on my thread, I’ve just been very busy these last few days. Trying to make sense of these posts is pretty much pointless at this moment, because I am fried. But I do understand what teen persuasion said about needing to plan for different stages of retirement. I’ve already been thinking about that because I will have different things going on at different times as far as income after retirement. I honestly don’t know much about Roth’s, not even the ones offered in my retirement account. I’m admittedly a big procrastinator, so I figured sticking the extra money in my traditional retirement account now, while it was on my mind, was better than waiting to do anything until I learned what I needed to know about Roth’s. I’m glad you all kept posting even though I was away. Thanks! The advantage to Roth accounts is that, once they are qualified, withdrawals from Roth are tax free. So having some of your retirement savings in Roth gives you some control over your tax bite in retirement years. If you need a bigger lump sum for a new roof, for example, you could draw it from Roth and it wouldn't bump your taxes up like a similar draw from a traditional account would. The obvious drawback to Roth accounts is that there's no tax break up front, so they "cost" more to fund. You have to guess whether it's better to prepay the tax (Roth) or delay the tax (traditional). It comes down to tax rates - are they higher now, or in retirement? You know your rate now, but in retirement is a guess, unless you can see some distinct reason it might be higher or lower in retirement. For most people, your retirement tax rate is probably going to be lower because income is probably lower - you aren't saving for retirement, maybe your mortgage is paid off, kids launched, and certain retirement income like SS is only partially taxed. But some people have higher taxes in retirement, perhaps because they have more income (pension + SS + RMDs) or because they could defer lots of income while working (so lower taxed income when working, but huge RMDs in retirement). You could even create a problem by leaning too heavily to one side - expect high retirement taxes, so go all Roth, now you owe zero tax in retirement (you overpaid tax) - or, expect low taxes, go all traditional, now huge RMDs and high tax (you deferred too much). If it's a crapshoot, you might want to hedge your bets by using some of each: some traditional for tax deferral now, some Roth for future tax free income. Look at the types of income you will have in retirement, and how they are taxed. Pensions and traditional account withdrawals will be taxed as ordinary income (like wages). SS is only partially taxable, but how much is taxable depends on that other income (more other income pushes more SS to become taxable). Roth withdrawals are tax free when qualified. So if you add up any pension + whatever you expect to withdraw from traditional accounts + up to 85% of SS, how does that compare to your current AGI? Higher might mean more taxes, lower might mean lower. Then extrapolate out - current traditional balances will grow, you will contribute more, etc. If you are already looking at higher taxes, you might want to get more Roth savings. You'd essentially be locking in today's lower tax cost. If you always will have lower retirement taxes, keep deferring to traditional accounts. If it's hard to predict, split the difference, do some of each. You may have noticed I used the word qualified several times about Roth IRA withdrawals. You can always withdraw contributions from Roth IRA accounts tax and penalty free at any time. But Roth earnings are not tax and penalty free until they are qualified. Essentially, that means you have had a Roth account for at least 5 tax years, and you are 59.5 or older. That 5 year clock is important, it's not just being over age 59.5 for tax free withdrawals. So you should open a Roth IRA to get that 5 year clock started. Oddly, it doesn't really need 5 years - you could open and fund an IRA on December 31 and have it count for that entire year - so it could be just a bit over 4 years to count thru 5 tax years. Roth IRA and Roth employer plans are not quite the same, either. I think you said you have TSP; Roth IRAs have no RMDs, ever. But Roth TSP or 401k, etc, do have RMDs. That means you have to withdraw from the account each year from 72 onward, whether you want to or not. You can get around this by rolling the whole account over to a Roth IRA (before RMDs start!). But it means you can't keep your investments in those great TSP funds. Tradeoffs. Another advantage of Roth IRAs over Roth employer plans is that ability to tap contributions at any time. Usually you can't withdraw from employer plans while you are still employed. A Roth IRA can be a backup emergency fund, not tied to your employer. So it could be good to continue contributing to your TSP for the match and tax deferral, and open a separate Roth IRA to start the 5 year clock ticking (so it's fully qualified when you hit 59.5) for any additional retirement savings. Then you have an additional tax free bucket for retirement. Thank you so much for explaining all of that. Especially for explaining why having a Roth IRA separate from what my employer offers in our retirement benefits could be better. |

|

tallguy

Senior Associate

Joined: Apr 2, 2011 19:21:59 GMT -5

Posts: 14,162

|

Post by tallguy on Mar 11, 2021 20:12:50 GMT -5

The big thing to remember is that as long as you keep saving and investing, you will have options. Yes, some options are better than others, both now and in the future. but at least you will have some. That alone puts you far ahead of many if not most of the people in this country. Learn about Roths. See where they fit into your plan. You will not get a tax break up front on the contributions, but it should probably be much more beneficial later on. Try to forecast as much as you can what your income and expenses are going to be in retirement, and at what age you want to leave the work world. Once you are able to do that you can ask more detailed questions and make more specific plans. In other words, KISS (keep it simple stupid) until you figure out what the heck you’re doing and need to do, right? I don’t say that in a negative way, because I think your advice is great, and I appreciate it. I’ve been meaning to learn more about Roths since I found these boards and saw you all talking about them. I just never felt a real sense of urgency, like I’m starting to feel now. I mean, at least I was saving for retirement, I thought I’d figure out the details later. Well, “later” is starting to feel like it should be “now”. And it sounds like you kind of said that I’m doing something half-way right by saving and investing in the first place, even though I haven’t figured out yet what I should have where, and I sincerely appreciate that too. I already know when I want to leave the working world. Tomorrow wouldn’t be too soon for me.😁 Realistically speaking though, I pray no later than 10 years from now. I want out literally as soon as possible, meaning whenever I can make the math make sense for the rest of my life. Without an early retirement offer with a financial incentive (which my employer has done in the past) that would be the earliest I think I can realistically retire, which is 2 years beyond when I would be eligible as far as my job goes. I’d shed real tears and be very, very unhappy if I had to work more than 10 more years. I have 6 more years before I would be eligible to take advantage of an early out with an incentive, if it was even offered. That would be awesome, but no matter what, for the love of all that is good and holy, PLEASE GOD, I don’t want to work my current job more than 10 more years. In 10 years and some months, I’ll be eligible to use the funds in my retirement account without penalty and receive my pension and the supplement. Anyway, you didn’t ask about all that. Just, thanks for the advice. Believe me, if you have been saving and investing for a number of years you are doing things far more than half-way right.  When I was young (teenager) I used to watch financial planning and advice shows when they came on during PBS pledge weeks. I figured that there may be only one minute during the course of that hour where I picked up something that I did not know before, but that I would have the benefit of that one minute for the rest of my life. It helped build a good foundation. Two things in particular I remember to this day, applicable mostly to new savers and investors. 1. 90% of financial planning is to spend less than you make. 2. Good financial planning is very simple stuff. It's the stuff that DOESN'T work that is complicated. You have time to learn how to optimize your situation and to learn better options and choices. The hard part was having the discipline to save the money in the first place. You obviously have the interest in learning more. Now is just following through. |

|

teen persuasion

Senior Member

Joined: Dec 20, 2010 21:58:49 GMT -5

Posts: 4,046

|

Post by teen persuasion on Mar 12, 2021 9:29:51 GMT -5

If you retire early and you need to purchase medical coverage on the market, you want to keep your income down in order to receive subsidies. The subsidies have a cliff to them. If you are $1 over 400% FPL, you get zero help. If you are below, you get help based on your level of income. Medical coverage can be very expensive depending on where you live. I'm not yet 60 and was paying $1000 per month for coverage with a $6500 deductible. That ate up our budget really quick. The newly signed legislation has removed the cliff, at least for a year or 2. You now pay no more than 8.5% of AGI for health insurance. |

|

Deleted

Joined: May 3, 2024 20:14:39 GMT -5

Posts: 0

|

Post by Deleted on Mar 12, 2021 9:34:54 GMT -5

The newly signed legislation has removed the cliff, at least for a year or 2. You now pay no more than 8.5% of AGI for health insurance. That's very good news although it doesn't affect me (I'm on Medicare). Cliffs are awful. |

|

buystoys

Junior Associate

Joined: Mar 30, 2012 4:58:12 GMT -5

Posts: 5,650

|

Post by buystoys on Mar 12, 2021 12:40:01 GMT -5

If you retire early and you need to purchase medical coverage on the market, you want to keep your income down in order to receive subsidies. The subsidies have a cliff to them. If you are $1 over 400% FPL, you get zero help. If you are below, you get help based on your level of income. Medical coverage can be very expensive depending on where you live. I'm not yet 60 and was paying $1000 per month for coverage with a $6500 deductible. That ate up our budget really quick. The newly signed legislation has removed the cliff, at least for a year or 2. You now pay no more than 8.5% of AGI for health insurance. Yes, that is good news. Unfortunately, DH and I paid through the nose for six years and are now, fortunately, both on Medicare. |

|

countrygirl2

Senior Associate

Joined: Dec 7, 2016 15:45:05 GMT -5

Posts: 16,930

|

Post by countrygirl2 on Mar 13, 2021 0:05:08 GMT -5

With medicare we are still paying near $1000 a month for insurance. We paid $400 when he was still working.

I got my taxes finished for my part. Balance sheet, P&L for the LLC. I don't drop numbers in, to many twists and turns, just know we will have to pay, just how much. Already paid in about $11k. Capital gains this year.

I didn't even think about the tax credit going against the monies for the increased in premiums, sigh. It's just hard to keep what you makes.

|

|

|

|

Post by The Walk of the Penguin Mich on Mar 13, 2021 0:33:29 GMT -5

With medicare we are still paying near $1000 a month for insurance. We paid $400 when he was still working.I got my taxes finished for my part. Balance sheet, P&L for the LLC. I don't drop numbers in, to many twists and turns, just know we will have to pay, just how much. Already paid in about $11k. Capital gains this year. I didn't even think about the tax credit going against the monies for the increased in premiums, sigh. It's just hard to keep what you makes. You were paying your share of the health insurance through your husband’s employer. That $400 was not the full cost of your insurance, it was probably closer to about $1600 for both of you. His employer picked up the balance as one of his benefits. If you were paying the full cost of health insurance for both you and your husband now, the cost would probably be well over $2000/mo. |

|

Deleted

Joined: May 3, 2024 20:14:39 GMT -5

Posts: 0

|

Post by Deleted on Mar 13, 2021 8:48:00 GMT -5

If you were paying the full cost of health insurance for both you and your husband now, the cost would probably be well over $2000/mo. I agree that employee health insurance is typically heavily-subsidized and your estimate of the cost of private insurance is about right (DB's employer dropped retiree healthcare 3 years ago and he and DSIL were paying $22K/year back then for ACA). Remember, though, that Medicare beneficiaries are paying for Part A their entire working lives. My employers and I paid in $120,000 over my career; accumulated at 6% that would be over $300,000. And now I'm paying IRMAA surcharges. |

|

CCL

Junior Associate

Joined: Jan 4, 2011 19:34:47 GMT -5

Posts: 7,599

|

Post by CCL on Mar 15, 2021 22:25:05 GMT -5

At what income do the IRMAA surcharges take effect?

|

|

|

|

Post by The Walk of the Penguin Mich on Mar 16, 2021 0:35:00 GMT -5

|

|

|

|

Post by minnesotapaintlady on Mar 16, 2021 8:02:32 GMT -5

I guess I can cross IRMAA off the list of things to worry about.

|

|

bean29

Junior Associate

Joined: Dec 19, 2010 22:26:57 GMT -5

Posts: 9,939

|

Post by bean29 on Mar 16, 2021 10:21:37 GMT -5

I was looking at your discussion on starting the clock ticking on a Roth IRA, and I just opened my Vanguard account up, called and told them I wanted to open a Roth IRA to start my clock ticking. It only took maybe 15 minutes. I just put $250 in it for now, but I am going to call back and open and account in DH's name too. I will do more in his name b/c he does not have access to a 401K.

ETA: I have some Roth investments in my 401K at work, but I never opened the traditional IRA to start the clock ticking. I have about $1500 in my 401K earmarked as ROTH, from several years ago, but then I went back to doing mostly traditional 401K. I just designated 10% of my 401K funds to go to ROTH in the future.

|

|

TheOtherMe

Distinguished Associate

Joined: Dec 24, 2010 14:40:52 GMT -5

Posts: 27,206

Mini-Profile Name Color: e619e6

|

Post by TheOtherMe on Mar 16, 2021 10:46:13 GMT -5

I guess I can cross IRMAA off the list of things to worry about. Same |

|

tallguy

Senior Associate

Joined: Apr 2, 2011 19:21:59 GMT -5

Posts: 14,162

|

Post by tallguy on Mar 16, 2021 11:59:48 GMT -5

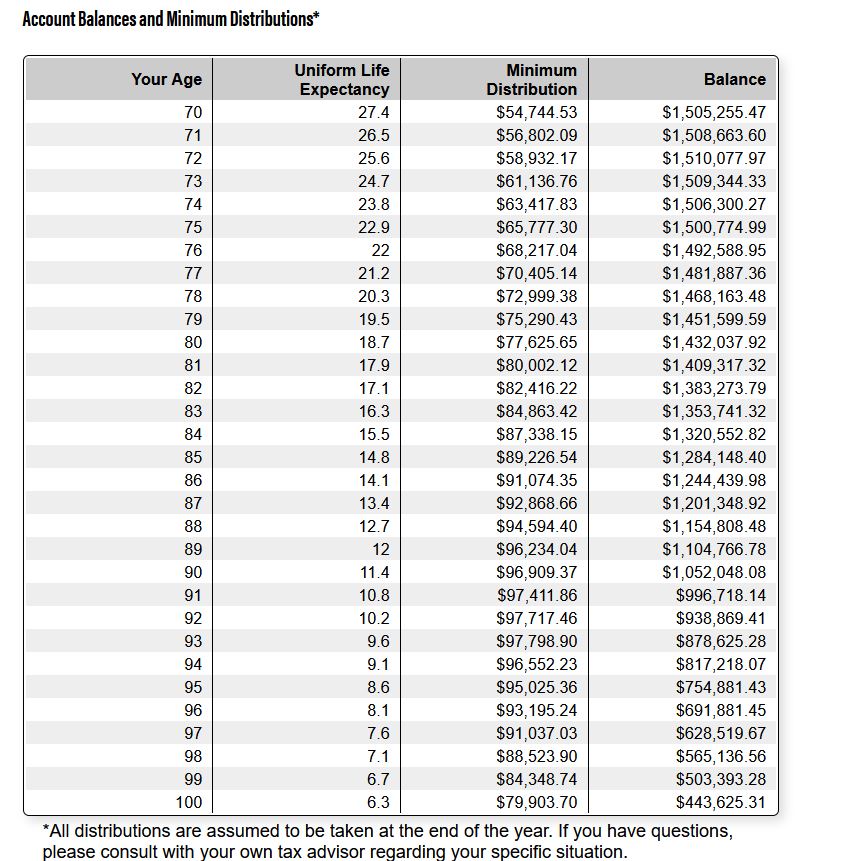

I guess I can cross IRMAA off the list of things to worry about. Under normal circumstances, perhaps.... I should not as a rule have to worry about it either, but there is one thing that I am thinking about. My situation changed in that I ended up taking SS at 60, earlier than planned. This meant that I could not do Roth conversions for as long a period as intended without making all of my SS taxable, resulting in my IRAs still being larger than I wanted them to be at this point. Because I am limiting my income for tax reasons, I cannot take more without causing myself a real problem. I realized that 2019 was the last year I could do a large conversion, so moved over $150,000 out of my IRA. I realized I would either never spend that money or would have to create a far larger tax hit for myself later to have access to it, so I paid a large tax bill up front to unlock all of that money. The issue now is that if I want to do another large conversion to get the IRA balances closer to where I want them, I have to do it this year or next. I would still pay a huge tax bill on the conversion, make the SS taxable, and lose the property tax exemption for a year, but it would make the excess IRA money available to me and decrease future RMDs. I would not, however, have to pay IRMAA surcharges because I would still be three years away from Medicare. If I wait, I would also have to pay IRMAA for a year or more in addition to the other costs. I have guessed that another $150,000 would cost me an additional $13,000 now on top of the tax on the conversion itself. That number will be even higher in the future. Adding IRMAA would increase it another few thousand. Because it doesn't make sense to convert at that level, I am going to be stuck with a lot of IRA money I will never spend. A nice problem to have, sure, but nicer still to have that money without paying a marginal rate over 40%. I guess my son will enjoy the money.  The bottom line is that getting your IRA balance in line with where you want it to be needs to be done early or it could cost you a lot more. I wanted mine to be down around $300,000, but am nowhere near that. Fortunately I do not need the money so can pass it along, but.... My GF also got hit with IRMAA. She was not aware of it and did a Roth conversion without asking me to review it so exceeded the threshold. Knows better now. Things can always pop up. It is far better to know about and understand things like IRMAA and never need that knowledge, than to not know and have it bite you. |

|

|

|

Post by minnesotapaintlady on Mar 16, 2021 12:16:35 GMT -5

tallguy - I guess I'll have to look at it more, but when I run the RMD calculators it doesn't seem so bad even on 1.5 million (although this is based on a 4% return) I don't foresee have 1.5 million. Probably not even 1 million so I'm not sure why I'd even care about doing large conversions? |

|

tallguy

Senior Associate

Joined: Apr 2, 2011 19:21:59 GMT -5

Posts: 14,162

|

Post by tallguy on Mar 16, 2021 12:44:11 GMT -5

tallguy - I guess I'll have to look at it more, but when I run the RMD calculators it doesn't seem so bad even on 1.5 million (although this is based on a 4% return) I don't foresee have 1.5 million. Probably not even 1 million so I'm not sure why I'd even care about doing large conversions? In my situation I want to keep my income (excluding Roth distributions but counting all SS) under $40,000. This means I can only take $10-13,000 per year out of my IRA without screwing myself up in taxes. That will never get my IRA balances low before RMDs hit, and I risk having the RMDs screw up my taxes every year a decade from now. Just the property tax exemption alone should save me about $8000 this year if I figured it correctly. That number will increase in the future, so I very much want to maintain it. (Add in the taxability of SS benefits and it is a few thousand more I would pay.) Not getting my IRA balance down will impact my ability to do that, hence the reason for a large conversion. I don't want to be in the position where being forced to take an extra $2000 RMD costs me $5000 in taxes, or an extra $15-20,000 in RMD costs me $10,000 in taxes every year. That is just bad planning. |

|

|

|

Post by minnesotapaintlady on Mar 16, 2021 13:05:31 GMT -5

tallguy - I guess I'll have to look at it more, but when I run the RMD calculators it doesn't seem so bad even on 1.5 million (although this is based on a 4% return) I don't foresee have 1.5 million. Probably not even 1 million so I'm not sure why I'd even care about doing large conversions? In my situation I want to keep my income (excluding Roth distributions but counting all SS) under $40,000. This means I can only take $10-13,000 per year out of my IRA without screwing myself up in taxes. That will never get my IRA balances low before RMDs hit, and I risk having the RMDs screw up my taxes every year a decade from now. Just the property tax exemption alone should save me about $8000 this year if I figured it correctly. That number will increase in the future, so I very much want to maintain it. (Add in the taxability of SS benefits and it is a few thousand more I would pay.) Not getting my IRA balance down will impact my ability to do that, hence the reason for a large conversion. I don't want to be in the position where being forced to take an extra $2000 RMD costs me $5000 in taxes, or an extra $15-20,000 in RMD costs me $10,000 in taxes every year. That is just bad planning. Gotcha. I forgot about your high property taxes and the exemption. Staying under 40K would be a lot more stressful with RMDs for sure. |

|

CCL

Junior Associate

Joined: Jan 4, 2011 19:34:47 GMT -5

Posts: 7,599

|

Post by CCL on Mar 16, 2021 13:36:43 GMT -5

I guess I can cross IRMAA off the list of things to worry about. Me, too. |

|