Tiny

Senior Associate

Joined: Dec 29, 2010 21:22:34 GMT -5

Posts: 13,399

|

Post by Tiny on Dec 18, 2014 15:28:42 GMT -5

I guess I was going to the point that just because some % of the employed don't have the ability to 'save' when they have access to an employer sponsered retirement plan doesn't mean that the problem is 100% with the plan. I realize that even with a 401(K) an employee might opt to have 100% of their saved money in a money market fund/account (ie a basic savings account or CD) because they are afraid to loose money OR they might have 100% of their money in their employers stock because 'hey! my employer is always going to make money!' This doesn't mean that 401(k)'s are bad or are somehow taking advantage of the average worker (which is what the article seems to imply). I see your point about ability to save. As far as 401k's taking advantage, yes and no. They were not intended to replace pensions at first. A bunch of well-compensated people wanted to have a tax shelter in which they could save for retirement, so the 401k was born for them. The average worker got taken for a ride when the 401k replaced their pension, yet they didn't get additional pay to put into the 401k. Matches tend to be pathetic. 7.5% would be awesome! The most I ever got was 4%. I've never had a "match" for employer 401(k)s. The first one I had my employer did a once a year "profit sharing" lump sum contribution. There were alot of rules/hoops to jump thru to be eligible for this contribution. It generally was from 2% to 3% of your salary. I contributed to that 401(k) for 14 years. My current employer offers a pension and a 401(k) with no match. I contribute to the 401(k). The other thing to consider is that 401(k) contributions are pretax money... so, yeah, someone earning 35K isn't in a particularly high tax bracket - but, I would imagine the actual out of pocket is a bit less than the actual contribution amount. And I would assume, no one is expecting them to be putting 17500 a year into their plan. That's for us over achieving YMer types.  Even if they were putting 1000 or so (3%) a year (that's $20 a week) over the course of 30 years - it would make a huge difference in their retirement. If as time goes by they upped it to 5% OR started to get an employer match they'd be in even better shape. Maybe I'm just out of touch - I'm apparently not as 'poor' as I think I am... (being single and having alot of DINK friends makes me feel poor). |

|

cronewitch

Junior Associate

Joined: Dec 20, 2010 21:44:20 GMT -5

Posts: 5,976

|

Post by cronewitch on Dec 18, 2014 15:47:28 GMT -5

When I was young before 401K plans often you got no pension money even if they had a pension. My boss was an elderly CPA so he gave us pension money until he was too old to contribute for himself I got a little money like a few hundred. I got a tiny amount working for a state once too but until I got 401K I had no control over retirement. I didn't get a 401K until the 90s and then not every job or every year, 2-5 years into a job they would start a 401K with a 15% limit and no match. I didn't get a decent one until 2003 when they allowed 14K instead of 15%. I still managed from 2003-2014 to save about 450K in that last 401K because they had profit sharing a few times of 7.5-15% on years we had a profit and I was over 50 so could put in a lot. I didn't worry so much about fees I just wanted to save so I could roll it when I retired.

|

|

Plain Old Petunia

Senior Member

bloom where you are planted

Joined: Dec 21, 2010 2:09:44 GMT -5

Posts: 4,840

|

Post by Plain Old Petunia on Dec 18, 2014 16:22:41 GMT -5

Not everyone had pensions in the first place.

|

|

Tiny

Senior Associate

Joined: Dec 29, 2010 21:22:34 GMT -5

Posts: 13,399

|

Post by Tiny on Dec 18, 2014 16:47:00 GMT -5

If your employer has a crappy 401(k) and no match - and you can't contribute more than 5K (the limit for Traditional IRAs) wouldn't it make sense to contribute to a personal IRA? At that low level of contribution (and no employer match) aren't the 'benefits' about equal? Yeah, you'd have to do alot more 'work' - like having internet access so you could open up an Account (not an IRA, but I did open an account at Fidelity all by mail back in the dark ages) and then have an automatic transfer set up or write/mail a check (I did this too back in the dark ages) - by, maybe, considering it a bill you had to pay. OK, I guess if you working for an employer that's paying you with a payroll debit card - or you can't get/keep a checking account you've got bigger fish to fry than trying to save in a tax advantaged account for retirement... But, for the people who have access to basic financial services - it's not that hard a bit inconvenient, sure. On the other hand - a friend 'fessed up to having opening an IRA at her bank and then having her contributions in what amounted to CDs held within the IRA.  You know what... nevermind... people are idiots and rolled in a coating of stupid... there's no hope. |

|

Deleted

Joined: Jul 8, 2024 14:45:34 GMT -5

Posts: 0

|

Post by Deleted on Dec 18, 2014 18:29:17 GMT -5

I feel sorry, though, for people trying to plan their retirement now at age 30 or so. Sure, the overachievers started with their high school job, but that's not most people.

$1,000,000 with the often advised 4% withdrawal rate is only $40,000 a year before taxes. If $40,000 a year before taxes doesn't feel like much now, think how little it will buy in the year 2050. Retirement is always a moving target, but even Phil admitted that some of the "growth" in the stock market is the result of inflation. A share of stock may triple in value, but if the cost of living has tripled, that isn't real growth. You are only staying even.

So those of you aiming for $1,000,000 might want to up that figure to $3,000,000. And that's just a guess! |

|

justme

Senior Associate

Joined: Feb 10, 2012 13:12:47 GMT -5

Posts: 14,618

|

Post by justme on Dec 18, 2014 19:30:10 GMT -5

If your employer has a crappy 401(k) and no match - and you can't contribute more than 5K (the limit for Traditional IRAs) wouldn't it make sense to contribute to a personal IRA? At that low level of contribution (and no employer match) aren't the 'benefits' about equal? Yeah, you'd have to do alot more 'work' - like having internet access so you could open up an Account (not an IRA, but I did open an account at Fidelity all by mail back in the dark ages) and then have an automatic transfer set up or write/mail a check (I did this too back in the dark ages) - by, maybe, considering it a bill you had to pay. OK, I guess if you working for an employer that's paying you with a payroll debit card - or you can't get/keep a checking account you've got bigger fish to fry than trying to save in a tax advantaged account for retirement... But, for the people who have access to basic financial services - it's not that hard a bit inconvenient, sure. On the other hand - a friend 'fessed up to having opening an IRA at her bank and then having her contributions in what amounted to CDs held within the IRA. You know what... nevermind... people are idiots and rolled in a coating of stupid... there's no hope. To be fair, I don't think you can contribute to a Traditional IRA if you have access to an employer plan. Or well, you can't contribute and deduct the contributions. There may be a income limit attached to that I'm not aware of. |

|

Plain Old Petunia

Senior Member

bloom where you are planted

Joined: Dec 21, 2010 2:09:44 GMT -5

Posts: 4,840

|

Post by Plain Old Petunia on Dec 18, 2014 19:31:33 GMT -5

I hate articles like this. First, just because you have access to one, doesn't mean it's like magic beans. Second, it just give those who aren't saving, or aren't saving much, another excuse not too. We have an employee that came in the other day to sign up for the 401K (finally). He's worked for us for 15 years, and is now 62. He went to an "investment guy" to talk about retirement and started to panic. The guy asked him why he was not in the employer plan and to go sign up immediately. His comment was " I guess I should have started sooner". mmm- yeah. Someone like him is going to see this article and it will convince them not to save. The author isn't doing anyone any favors. I agree. And I just noticed the author is Helaine Olen. I disagree with most of her opinions.

|

|

Deleted

Joined: Jul 8, 2024 14:45:34 GMT -5

Posts: 0

|

Post by Deleted on Dec 18, 2014 21:52:52 GMT -5

Some people just don't have the self-control to save, despite their intelligence and ability to understand investing. Others feel like they can't possibly understand it even though they could. They just have a mental block when it comes to math, which would extend to investing. My Ex was brilliant when it came to inorganic chemistry and clueless about finances. He also had exquisite taste and no discipline. But to get back to the OT- I agree that in many companies, replacing a DB pension with a 401(k) was definitely a bait-and-switch. It's especially true when they provided no match and had crappy funds with high expense ratios. Having said that- there are plenty of reasons not to save. The market is rigged. The 401(k) options are lousy. Crashes happen. So I guess for many people the solution is to spend it all. Sorry, I'm not buying it. You can save outside of the 401(k). If the 401(k) options are bad, use the money market options to get the match and be more aggressive with your after-tax investments. If you're withdrawing 4% or less, a 10% or even a 25% drop won't cramp your style much and you can wait for it to recover. |

|

tallguy

Senior Associate

Joined: Apr 2, 2011 19:21:59 GMT -5

Posts: 14,289

|

Post by tallguy on Dec 18, 2014 22:41:01 GMT -5

Yes, you can (up to a certain income limit.) It depends on your modified AGI and your filing status. Here is the link from the IRS. For a single person the phaseout range for 2014 is between $60,000-$70,000.

Trust me, you do NOT want to know how extreme someone can get with that.

|

|

TheHaitian

Senior Associate

Joined: Jul 27, 2014 19:39:10 GMT -5

Posts: 10,144

|

Post by TheHaitian on Dec 19, 2014 3:24:25 GMT -5

Well.... you do fit the bill, don't you? You are struggling with DW (maybe not so much any more?) to get on the same page and save more right? I'm not saying there's anything right or wrong about it, but you ARE pretty solidly mid-upper class and you DO shop at Pottery Barn... right? A couple making $120,000/year would need to save up to 30% of their gross income to max two 401k's/403b's to the tune of $36,000. I am nowhere near the upper class when you consider the makeup of HCOLA of Massachusetts. More like middle class, make enough to afford all our needs and some of our wants. Yes we shop at those places but it is not like we are there "everyday" and believes that is not what is keeping the middle class from saving. I will say for a couple like us starting out: - high housing costs - transportation costs and/or car costs - daycare Those are the things eating the money before it gets to the 401k.... |

|

tallguy

Senior Associate

Joined: Apr 2, 2011 19:21:59 GMT -5

Posts: 14,289

|

Post by tallguy on Dec 19, 2014 3:27:13 GMT -5

I REALLY hope that is the other way around....

|

|

TheHaitian

Senior Associate

Joined: Jul 27, 2014 19:39:10 GMT -5

Posts: 10,144

|

Post by TheHaitian on Dec 19, 2014 3:29:26 GMT -5

I REALLY hope that is the other way around....

Fixed 3 AM... No coffee yet... Don't judge me  |

|

tallguy

Senior Associate

Joined: Apr 2, 2011 19:21:59 GMT -5

Posts: 14,289

|

Post by tallguy on Dec 19, 2014 3:32:50 GMT -5

Good, but judging from some of the things we've had to read about your wife it could have gone either way.  |

|

thyme4change

Community Leader

Joined: Dec 26, 2010 13:54:08 GMT -5

Posts: 40,510

|

Post by thyme4change on Dec 19, 2014 8:16:27 GMT -5

I read until the part where she said "Most workers have absolutely nothing left from their paycheck to save." (A quote from someone at the beginning of the 401k.)

I look at what I spent my money on in 1993 and what young people spend their money on now - there is money left over. Home phones were like $18 a month, and now cell plans are $100+. Everyone found money to get one of those. Internet and computers cost us $0.00 in 1993 and now everyone spends $50 a month on those. Hulu plus cost more per month than I spent in a year to watch television back in the day.

I'm not saying that buying any of those things is bad, or that they aren't pretty key to having a normal life these days. I'm just saying that the general population seems to find money in their budget for all kinds of things, but we all cry poor when we are expected to take care of ourselves and our future.

|

|

resolution

Junior Associate

Joined: Dec 20, 2010 13:09:56 GMT -5

Posts: 7,058

Mini-Profile Name Color: 305b2b

|

Post by resolution on Dec 19, 2014 8:24:03 GMT -5

I read until the part where she said "Most workers have absolutely nothing left from their paycheck to save." (A quote from someone at the beginning of the 401k.) I look at what I spent my money on in 1993 and what young people spend their money on now - there is money left over. Home phones were like $18 a month, and now cell plans are $100+. Everyone found money to get one of those. Internet and computers cost us $0.00 in 1993 and now everyone spends $50 a month on those. Hulu plus cost more per month than I spent in a year to watch television back in the day. I'm not saying that buying any of those things is bad, or that they aren't pretty key to having a normal life these days. I'm just saying that the general population seems to find money in their budget for all kinds of things, but we all cry poor when we are expected to take care of ourselves and our future. The sad thing is that my friends that don't save will lecture me for not having the fancy phone and cable tv, or they stage interventions to try to bring me into the 20th century. I don't understand why it is so important to them. Even sadder is that I finally bought the phone, and now it is sitting here while I procrastinate on getting it activated. |

|

973beachbum

Senior Associate

Politics Admin

Joined: Dec 17, 2010 16:12:13 GMT -5

Posts: 10,501

|

Post by 973beachbum on Dec 19, 2014 9:15:53 GMT -5

I just want to say that I graduated college in 87. All the retirement planning talked about the Three legged Stool. The 401K was a replacement of the personal savings though NOT the pensions. Last I checked I can't use the same money twice. So if the amount I used to put in a personal savings account now goes to the 401K it can't then also be used to put into the company 401K. And just for the record I never worked for a company that had a 401K match although I haven't worked for a company with a 401K in while either. |

|

shanendoah

Senior Associate

Joined: Dec 18, 2010 19:44:48 GMT -5

Posts: 10,096

Mini-Profile Name Color: 0c3563

|

Post by shanendoah on Dec 19, 2014 11:15:43 GMT -5

973beachbum - I'm trying to understand what you're saying. If you put money into a personal 401(k) it can't go into the company 401(k)? I didn't think there were such things as personal 401(k)s.

Also, you're saying the 401(k) was supposed to replace personal savings, so the pension was supposed to stick around? (I'm guessing the 3rd leg was social security.)

So when did that change? When did companies decided that the 401(k) needed to replace BOTH personal savings and pensions? Or was it decided that never mind, you needed to save twice- once in the company 401(k) to replace the pension, and once in traditional IRAs/money market accounts, etc to cover your retirement?

|

|

HoneyBBQ

Junior Associate

Joined: Dec 27, 2010 10:36:09 GMT -5

Posts: 5,395

Mini-Profile Background: {"image":"","color":"3b444e"}

|

Post by HoneyBBQ on Dec 19, 2014 11:41:33 GMT -5

I haven't looked at my balances lately. Maybe I should and I'll feel better lol.

|

|

Tiny

Senior Associate

Joined: Dec 29, 2010 21:22:34 GMT -5

Posts: 13,399

|

Post by Tiny on Dec 19, 2014 12:00:44 GMT -5

973beachbum - I'm trying to understand what you're saying. If you put money into a personal 401(k) it can't go into the company 401(k)? I didn't think there were such things as personal 401(k)s.

Also, you're saying the 401(k) was supposed to replace personal savings, so the pension was supposed to stick around? (I'm guessing the 3rd leg was social security.)

So when did that change? When did companies decided that the 401(k) needed to replace BOTH personal savings and pensions? Or was it decided that never mind, you needed to save twice- once in the company 401(k) to replace the pension, and once in traditional IRAs/money market accounts, etc to cover your retirement? The '3 legged stool' is Pension, SS, Personal Savings. There are quite a few retirees who currently have a 4 legged stool - Pension, SS, 401(k) or some other type of employer 'account', and then personal savings. I think at some point in the future the 3 legged stool will be SS, 401(k) or some other kind of retirement plan funded by the employee, and personal savings. If my retirement was 30 years or more out into the future (ie someone young and working) - I would be working/saving/investing with that in mind - that I wouldn't have Pension. I don't want to put words into 973BeachBum's mouth but what I suspect she's saying is that now a days - the employee is expected to FUND both an Employer sponsered plan (401k) (or an IRA/ROTH IRA) AND personal savings. If someone can save 5% per year - they have to choose how to split that up between retirement and personal savings. So, in the long run employers potentially (if they don't offer a match) aren't really contributing anything to an employee's retirement. The employee is responsible for 2 legs of the retirement stool. Which in turn means less disposable income.  Also, I think Beach is calling a traditional IRA a "personal 401(k)" |

|

gooddecisions

Senior Member

Joined: Dec 22, 2010 13:42:28 GMT -5

Posts: 2,418

|

Post by gooddecisions on Dec 19, 2014 12:08:00 GMT -5

I read until the part where she said "Most workers have absolutely nothing left from their paycheck to save." (A quote from someone at the beginning of the 401k.) I look at what I spent my money on in 1993 and what young people spend their money on now - there is money left over. Home phones were like $18 a month, and now cell plans are $100+. Everyone found money to get one of those. Internet and computers cost us $0.00 in 1993 and now everyone spends $50 a month on those. Hulu plus cost more per month than I spent in a year to watch television back in the day. I'm not saying that buying any of those things is bad, or that they aren't pretty key to having a normal life these days. I'm just saying that the general population seems to find money in their budget for all kinds of things, but we all cry poor when we are expected to take care of ourselves and our future. Sure you could make that argument, but you could also argue the other way...(Disclaimer, I am not a liberal, but even I can see the problem). Joe Middle Class has a $50K/year job. 15% goes to a 401(k)= $7500 10% to IRA= $5K 10% for health insurance premium= $5K 10% to HSA/FSA= $5K 45% of your income is gone and by the time taxes (all of them) are taken out- you're left with what? 40% of your income before any of your housing, food, childcare or transportation needs are paid. So, Joe Middle Class drops his retirement down to 5% to get the company match and funds an IRA some years if it was a good year. He skips the HSA and falls into debt when he has minor medical issue now that the deductibles and co-insurance is more expensive than ever. His retirement is way underfunded. And, yeah, he whines about how expensive everything while multi-tasking on his iphone 5. I don't have HULU, netflex or even a cell phone, but I don't begrudge anyone who does. It's frustrating doing the right thing with your money, just so you can't not afford a measly cell phone plan or cable plan. You can't just expect everyone to have a mind shift when it comes to t.v. and phones. If people could afford them since the day they were invented, well why shouldn't they still be able to afford them. Oh yeah, because employers used to fund benefits like retirement and insurance, but don't anymore. And, now not everyone has figured out how to afford everything thus retirement and insurance have become negotiable since folks reason that they government, family, _____ will take care of them. Edited to make it easier to read. |

|

Deleted

Joined: Jul 8, 2024 14:45:34 GMT -5

Posts: 0

|

Post by Deleted on Dec 19, 2014 12:24:49 GMT -5

I read until the part where she said "Most workers have absolutely nothing left from their paycheck to save." (A quote from someone at the beginning of the 401k.) I look at what I spent my money on in 1993 and what young people spend their money on now - there is money left over. Home phones were like $18 a month, and now cell plans are $100+. Everyone found money to get one of those. Internet and computers cost us $0.00 in 1993 and now everyone spends $50 a month on those. Hulu plus cost more per month than I spent in a year to watch television back in the day. I'm not saying that buying any of those things is bad, or that they aren't pretty key to having a normal life these days. I'm just saying that the general population seems to find money in their budget for all kinds of things, but we all cry poor when we are expected to take care of ourselves and our future. Sure you could make that argument, but you could also argue the other way...(Disclaimer, I am not a liberal, but even I can see the problem). Joe Middle Class has a $50K/year job. 15% goes to a 401(k)= $7500 10% to IRA= $5K 10% for health insurance premium= $5K 10% to HSA/FSA= $5K 45% of your income is gone and by the time taxes (all of them) are taken out- you're left with what? 40% of your income before any of your housing, food, childcare or transportation needs are paid. So, Joe Middle Class drops his retirement down to 5% to get the company match and funds an IRA some years if it was a good year. He skips the HSA and falls into debt when he has minor medical issue now that the deductibles and co-insurance is more expensive than ever. His retirement is way underfunded. And, yeah, he whines about how expensive everything while multi-tasking on his iphone 5. I don't have HULU, netflex or even a cell phone, but I don't begrudge anyone who does. It's frustrating doing the right thing with your money, just so you can't not afford a measly cell phone plan or cable plan. You can't just expect everyone to have a mind shift when it comes to t.v. and phones. If people could afford them since the day they were invented, well why shouldn't they still be able to afford them. Oh yeah, because employers used to fund benefits like retirement and insurance, but don't anymore. And, now not everyone has figured out how to afford everything and retirement and insurance have become negotiable. Edited to make it easier to read. But that person making 50K doesn't need to save $17,500/year to be saving adequately for retirement (assuming we're not talking someone that is trying to play catch-up). |

|

gooddecisions

Senior Member

Joined: Dec 22, 2010 13:42:28 GMT -5

Posts: 2,418

|

Post by gooddecisions on Dec 19, 2014 12:52:48 GMT -5

Sure you could make that argument, but you could also argue the other way...(Disclaimer, I am not a liberal, but even I can see the problem). Joe Middle Class has a $50K/year job. 15% goes to a 401(k)= $7500 10% to IRA= $5K 10% for health insurance premium= $5K 10% to HSA/FSA= $5K 45% of your income is gone and by the time taxes (all of them) are taken out- you're left with what? 40% of your income before any of your housing, food, childcare or transportation needs are paid. So, Joe Middle Class drops his retirement down to 5% to get the company match and funds an IRA some years if it was a good year. He skips the HSA and falls into debt when he has minor medical issue now that the deductibles and co-insurance is more expensive than ever. His retirement is way underfunded. And, yeah, he whines about how expensive everything while multi-tasking on his iphone 5. I don't have HULU, netflex or even a cell phone, but I don't begrudge anyone who does. It's frustrating doing the right thing with your money, just so you can't not afford a measly cell phone plan or cable plan. You can't just expect everyone to have a mind shift when it comes to t.v. and phones. If people could afford them since the day they were invented, well why shouldn't they still be able to afford them. Oh yeah, because employers used to fund benefits like retirement and insurance, but don't anymore. And, now not everyone has figured out how to afford everything and retirement and insurance have become negotiable. Edited to make it easier to read. But that person making 50K doesn't need to save $17,500/year to be saving adequately for retirement (assuming we're not talking someone that is trying to play catch-up). He was never saving $17500. |

|

Deleted

Joined: Jul 8, 2024 14:45:34 GMT -5

Posts: 0

|

Post by Deleted on Dec 19, 2014 13:03:24 GMT -5

But that person making 50K doesn't need to save $17,500/year to be saving adequately for retirement (assuming we're not talking someone that is trying to play catch-up). He was never saving $17500. I guess I'm confused by the initial percentages. I assumed it was what you thought he "should" be saving. |

|

Tiny

Senior Associate

Joined: Dec 29, 2010 21:22:34 GMT -5

Posts: 13,399

|

Post by Tiny on Dec 19, 2014 13:10:03 GMT -5

But that person making 50K doesn't need to save $17,500/year to be saving adequately for retirement (assuming we're not talking someone that is trying to play catch-up). He was never saving $17500. But your example shows what it would be like if he did save $17500 employer plan, personal Roth, and then HSA. these guys are all potentially "retirement savings" - yeah the HSA is debateable - the FSA is definitely NOT since it has a life span of 1 year (more or less). 15% goes to a 401(k)= $7500 10% to IRA= $5K 10% to HSA/FSA= $5K Someone making 50K should probably contribute 10% to their employer 401(k). If there's a match - they should meet the requirements for the match - and then decide what to do with what's left over - the 401(k) OR the HSA (if they are healthy and CAN let the money grow in the HSA) or some other retirement option. Either way they should be planning to have 5K of their income going into some sort of long term retirement savings - hopefully some of it is pre tax (thus giving them alittle extra bang for their buck). As has been pointed out someone earning 50K doesn't need to be saving 20 or 30% of their income for retirement UNLESS they truly want to be 'retired' by 50 or 55 (or sooner) and if that's the case - they probably shouldn't be saving all that money in accounts they can't access easily or without penalties before they are of true retirement age.... If they consistently save 10% for 20 or 30 years - and choose some sort of investment that atleast keeps up with inflation or better yet exceeds inflation they shouldn't be too poorly off in retirement. If they can 'sock away' some more money - either via an HSA, or personal savings or maybe even a house they've owned for 30 years their retirement looks better. All of the above assumptions are that the person is younger and has 20 or 30 or 40 years to 'invest' |

|

Lizard Queen

Senior Associate

103/2024

Joined: Jan 17, 2011 22:19:13 GMT -5

Posts: 14,659

|

Post by Lizard Queen on Dec 19, 2014 13:18:27 GMT -5

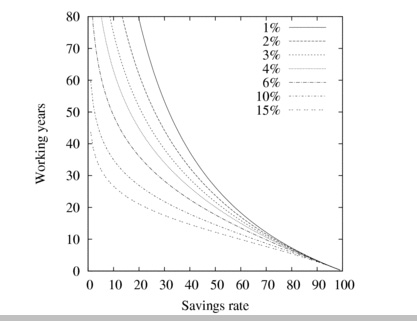

He was never saving $17500. But your example shows what it would be like if he did save $17500 employer plan, personal Roth, and then HSA. these guys are all potentially "retirement savings" - yeah the HSA is debateable - the FSA is definitely NOT since it has a life span of 1 year (more or less). 15% goes to a 401(k)= $7500 10% to IRA= $5K 10% to HSA/FSA= $5K Someone making 50K should probably contribute 10% to their employer 401(k). If there's a match - they should meet the requirements for the match - and then decide what to do with what's left over - the 401(k) OR the HSA (if they are healthy and CAN let the money grow in the HSA) or some other retirement option. Either way they should be planning to have 5K of their income going into some sort of long term retirement savings - hopefully some of it is pre tax (thus giving them alittle extra bang for their buck). As has been pointed out someone earning 50K doesn't need to be saving 20 or 30% of their income for retirement UNLESS they truly want to be 'retired' by 50 or 55 (or sooner) and if that's the case - they probably shouldn't be saving all that money in accounts they can't access easily or without penalties before they are of true retirement age.... 10% get's you to retirement in 51 years. That's over 70 for someone who starts at 20.  www.mrmoneymustache.com/2012/01/13/the-shockingly-simple-math-behind-early-retirement/ www.mrmoneymustache.com/2012/01/13/the-shockingly-simple-math-behind-early-retirement/ |

|

Deleted

Joined: Jul 8, 2024 14:45:34 GMT -5

Posts: 0

|

Post by Deleted on Dec 19, 2014 13:22:29 GMT -5

But your example shows what it would be like if he did save $17500 employer plan, personal Roth, and then HSA. these guys are all potentially "retirement savings" - yeah the HSA is debateable - the FSA is definitely NOT since it has a life span of 1 year (more or less). 15% goes to a 401(k)= $7500 10% to IRA= $5K 10% to HSA/FSA= $5K Someone making 50K should probably contribute 10% to their employer 401(k). If there's a match - they should meet the requirements for the match - and then decide what to do with what's left over - the 401(k) OR the HSA (if they are healthy and CAN let the money grow in the HSA) or some other retirement option. Either way they should be planning to have 5K of their income going into some sort of long term retirement savings - hopefully some of it is pre tax (thus giving them alittle extra bang for their buck). As has been pointed out someone earning 50K doesn't need to be saving 20 or 30% of their income for retirement UNLESS they truly want to be 'retired' by 50 or 55 (or sooner) and if that's the case - they probably shouldn't be saving all that money in accounts they can't access easily or without penalties before they are of true retirement age.... 10% get's you to retirement in 51 years. That's over 70 for someone who starts at 20. www.mrmoneymustache.com/2012/01/13/the-shockingly-simple-math-behind-early-retirement/That's ignoring the 5% company match and assuming only a 5% return during the working years. |

|

973beachbum

Senior Associate

Politics Admin

Joined: Dec 17, 2010 16:12:13 GMT -5

Posts: 10,501

|

Post by 973beachbum on Dec 19, 2014 13:27:51 GMT -5

973beachbum - I'm trying to understand what you're saying. If you put money into a personal 401(k) it can't go into the company 401(k)? I didn't think there were such things as personal 401(k)s.

Also, you're saying the 401(k) was supposed to replace personal savings, so the pension was supposed to stick around? (I'm guessing the 3rd leg was social security.)

So when did that change? When did companies decided that the 401(k) needed to replace BOTH personal savings and pensions? Or was it decided that never mind, you needed to save twice- once in the company 401(k) to replace the pension, and once in traditional IRAs/money market accounts, etc to cover your retirement? No. what I was trying to say, although badly obviously , is the old three legged stool was made up of pensions, SS and personal savings. When 401K's came about they were supposed to be a vehicle for personal savings. I'm sure this had more to do with high earning people who wanted a tax free vehicle but that is another story. Has anyone ever tried to sit on a two legged stool? Kinda makes the point visually I think.  ETA just forget what I said and read Tiny's. She said it so much better than I did! |

|

Lizard Queen

Senior Associate

103/2024

Joined: Jan 17, 2011 22:19:13 GMT -5

Posts: 14,659

|

Post by Lizard Queen on Dec 19, 2014 13:29:26 GMT -5

That's ignoring the 5% company match and assuming only a 5% return during the working years. That's 5% after inflation. Pretty reasonable assumption, IMO. I always ignore the company match. There are too many ways to be screwed out of it--vesting schedule, dropping in hard times, timing of when it is transferred, etc. |

|

HoneyBBQ

Junior Associate

Joined: Dec 27, 2010 10:36:09 GMT -5

Posts: 5,395

Mini-Profile Background: {"image":"","color":"3b444e"}

|

Post by HoneyBBQ on Dec 19, 2014 13:34:11 GMT -5

"If you save a reasonable percentage of your take-home pay, like 50%, and live on the remaining 50%, you’ll be Ready to Rock (aka “financially independent”) in a reasonable number of years"

From Mr Money Mustache's link.   I mean, I guess there are people who live on 50% take home. But: -this ignores that a large % of people's salaries goes to retirement (pre tax, not take home) - expenses change dramatically when you stop working in many cases\ - I could go on...

|

|

Deleted

Joined: Jul 8, 2024 14:45:34 GMT -5

Posts: 0

|

Post by Deleted on Dec 19, 2014 13:34:14 GMT -5

That's ignoring the 5% company match and assuming only a 5% return during the working years. That's 5% after inflation. Pretty reasonable assumption, IMO. I always ignore the company match. There are too many ways to be screwed out of it--vesting schedule, dropping in hard times, timing of when it is transferred, etc. It also seems to be ignoring SS. Someone making 50K could get a third of their expenses replaced with SS. |

|